The real cost of "Custom-built" insurance platforms (vs. Configurable Cloud Cores)

Intro

For many insurers, building a custom platform feels like the safest choice.

Full control.

Exact fit.

No vendor limitations.

On paper, it sounds logical.

In practice, custom-built insurance systems often cost far more than expected — not upfront, but over time.

And the cost isn't just financial.

It's measured in:

1. Speed lost

2. Flexibility sacrificed

3. Teams burned out

4. Opportunities missed

Let's talk about what nobody puts in the business case.

Why custom builds look so attractive

Custom development usually starts with good intentions — and real pain points:

"Our products are too unique for off-the-shelf platforms."

"Vendors force us into their way of doing things."

"We need complete control over our logic and data."

Especially for insurers with:

– Complex portfolios (multiple lines of business, hybrid products)

– Regional specifics (local regulations, unique distribution models)

– Legacy integrations (decades of accumulated systems)

... building in-house feels like the only way to protect flexibility.

And at the beginning?

It often works.

The first product launches.

The team is motivated.

Everything feels possible.

Then reality arrives.

The costs that rarely appear in the business case

The real trade-offs tend to surface 6 –18 months after go-live.

Not with a bang.

With a slow accumulation of friction.

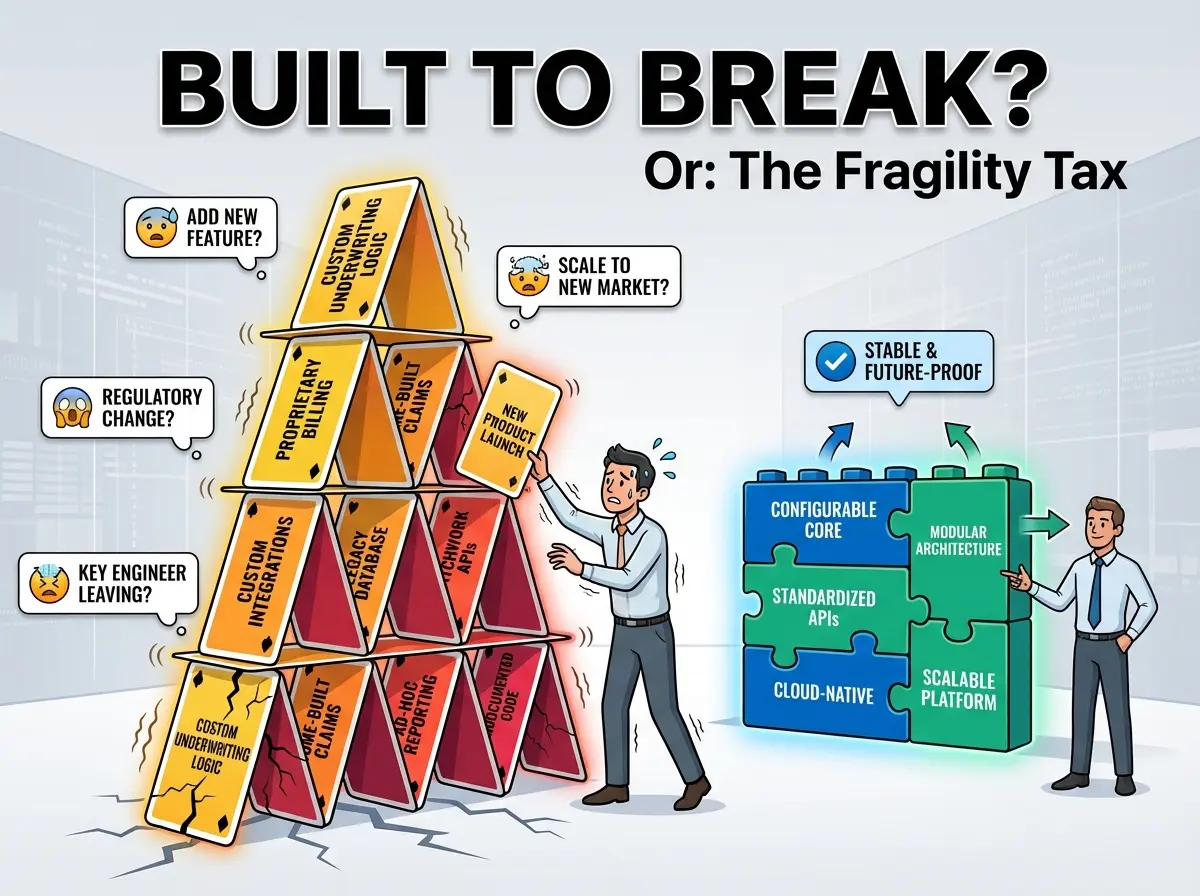

1. Change becomes expensive (and slow)

Every insurance business changes constantly:

– Pricing rules evolve (competitive pressure, loss ratios)

– Regulations update (data protection, reporting requirements)

– Distribution expands (new channels, embedded insurance, partnerships)

– Customer expectations shift (digital-first, instant quotes, self-service)

In custom systems, every change is a development project.

What started as "we control everything" slowly turns into dependency on:

– Specific engineers ("only Alex knows how underwriting works")

– Undocumented logic ("we think this was for the 2019 regulator audit")

– Brittle integrations ("if we touch that, three other things break")

We have seen this pattern across Eastern Europe, MENA, and the Caucasus:

An insurer launches a custom platform.

Year one — everything is new and exciting.

Year two — launching a simple product variant takes 3 months and 5 sprints.

Year three — the team is afraid to change anything.

That's not flexibility.

That's fragility.

2. Teams become the platform

Over time, knowledge concentrates.

Only a few people understand how things really work.

1. Onboarding new engineers takes months (not weeks)

2. Code reviews become bottlenecks ("we need Maria to approve this")

3. Leaving team members take critical context with them

At that point, the platform is no longer an asset.

It's a liability held together by institutional memory.

And when those key people leave?

You are not just losing employees.

You are losing the platform's operating manual.

3. Regulatory pressure multiplies complexity

Insurance platforms don't exist in isolation.

They must continuously respond to:

– Reporting requirements (monthly, quarterly, ad-hoc audits)

– Audit trails (who changed what, when, and why)

– Data residency rules (where data lives, how it moves)

– Security standards (encryption, access control, pen testing)

Custom platforms often handle compliance reactively:

New regulation comes?

Add a patch.

New audit requirement?

Build an export script.

New security standard?

Bolt on another layer.

This increases both operational risk and maintenance cost exponentially.

We have seen custom platforms where:

1. 40% of development time goes to compliance patches

2. Audit reports require manual data extraction from 5 different databases

3. Security updates break existing workflows

Compliance isn't a feature you add.It's an architecture you design for.

When custom development actually makes sense

To be clear — custom development isn't always wrong.

It can be justified when:

1. The business model is genuinely experimental

You're testing something nobody has done before. Fine. Build it custom. Learn fast.

2. The scope is narrow and well-contained

A specific API, a data connector, a reporting module. Custom code for specific problems? Often the right call.

3. Long-term ownership costs are fully understood

You have a dedicated team, clear documentation standards, and budget for continuous maintenance. Rare, but possible.

The problem isn't custom code itself.

It's using custom builds for core operational systems that must:

1. Scale (10x volume, new markets, new products)

2. Comply (changing regulations, audits, security)

3. Evolve (continuously, safely, without constant rewrites)

Core systems need stability, not constant surgery.

Why configurable cloud cores change the equation

Modern cloud-based insurance cores are designed around a different principle:

Configurability instead of constant redevelopment.

That means:

Products are defined through parameters, not code

Launch a new product variant? Configuration, not development sprint.

Workflows adapt without rewriting logic

Change commission structure? Adjust rules, not rewrite modules.

Integrations follow standardized APIs

Connect new payment gateway? Standard API, not custom plumbing.

Compliance is embedded, not added later

Audit trails, data residency, security? Built-in from day one.

The result isn't less control.

It's control without fragility.

You can still adapt.

You can still differentiate.

You can still own your logic.

But you're not rebuilding the engine every time you need to change direction.

How CLP Hub fits into this model

CLP Hub is built as a configurable insurance core, not a black-box SaaS.

This means insurers can:

✅ Launch quickly (3–6 months, not 18+)

✅ Adapt products safely (business teams configure, not IT rebuilds)

✅ Scale across markets (multi-country, multi-currency, multi-language out of the box)

✅ Reduce dependency on custom development (use it where it adds value, not where it creates risk)

Customization still exists.

But it's applied where it creates competitive advantage — not where it creates technical debt.

Examples:

1. Custom pricing algorithms? Plug them in via API.

2. Unique underwriting rules? Configure them in the rules engine.

3. Specific integrations? Standard connectors handle 80%, custom code handles the 20% that matters.

We have seen teams at insurers and banks move from saying

“We need six months to launch a product variant”

to confidently shipping and testing the same change in just two weeks.

Not because they gave up control.

But because they stopped rebuilding the same infrastructure over and over.

Real example — what "configurable" actually looks like

Let's say you're a Tier-2 insurer in MENA.

You want to launch auto insurance in a new country.

Custom-built platform approach:

- Developer writes country-specific logic (2 weeks)

- QA tests edge cases (1 week)

- Regulatory review requires changes (1 week)

- Deploy and pray nothing breaks (1 week)

- Total: 5+ weeks, high risk

Configurable platform approach (CLP Hub):

- Configure product parameters (country, currency, coverage types) — 2 days

- Map local regulatory requirements to built-in compliance framework — 3 days

- Test workflows with real scenarios — 1 week

- Go live — 2 weeks total, low risk

Same result. 60% faster. No custom code.

And when regulations change?

You adjust configuration, not rewrite code.

The hidden ROI — what you don't have to pay for

When evaluating custom vs. configurable, most business cases miss the negative costs — things you DON'T have to pay for with configurable platforms:

❌ Developer time spent on "plumbing" instead of features

❌ Months of onboarding for new engineers

❌ Crisis meetings when key people leave

❌ Emergency patches when regulations change

❌ Manual workarounds because "the system can't do that"

❌ Projects delayed because "we're still maintaining the old stuff"

These costs never appear in the business case.

But they consume years.

Final thought

The real cost of custom-built platforms isn't visible in year one.

It appears:

1. When volumes grow (and the system can't scale)

2. When teams change (and knowledge walks out the door)

3. When regulations tighten (and compliance becomes a bottleneck)

4. When speed matters again (and every change takes months)

The question is no longer:

"Can we build this ourselves?"

It's:

"Can we afford to keep rebuilding it?"

Most insurers don't fail because they chose custom.

They fail because they treated core systems like projects — not platforms.

Platforms need to evolve, scale, and survive — without constant surgery.

That's what configurable cores are built for.

Thinking about custom vs. configurable?

We've helped insurers across MENA, Eastern Europe, and the Caucasus navigate this exact decision.

Let's compare notes — what works, what doesn't, and what fits your situation.

Get in touch and request a demo.